Payroll in Indonesia can be challenging due to changing tax rules each year. Even minor adjustments to income brackets, relief programs, or deductions influence monthly withholding. Hence, many companies rely on a personal income tax calculator, but accuracy still depends on understanding how PPh 21 actually works.

This guide explains the updated rules for 2026 and the practical steps needed to calculate PPh 21 correctly.

Understanding personal income tax (PPh 21) in Indonesia

Payroll mistakes often begin with uncertainty around how PPh 21 should be applied in real situations. Companies generally understand what income tax is, but the practical application of new brackets, exemptions, and allowable deductions can create inconsistencies in payroll results.

In Indonesia, PPh 21 is the tax withheld from an employee’s income. It applies to salaries, fixed allowances, variable benefits, and other compensation that falls under the local tax framework. The difficulty usually comes from understanding how updated rules influence:

- The income that must be taxed

- The income that may be excluded

- The correct withholding amount is calculated each month

When these areas are clarified, payroll becomes more consistent, and tools such as a personal income tax calculator yield more accurate results.

Personal income tax rate in Indonesia

Indonesia uses a five-tier progressive structure, known legally as Tarif Progresif PPh Pasal 17, which remains valid through 2026.

- 5% for taxable income up to IDR 60 million

- 15% for income above IDR 60 million up to IDR 250 million

- 25% for income above IDR 250 million up to IDR 500 million

- 30% for income above IDR 500 million up to IDR 5 billion

- 35% for income exceeding IDR 5 billion

Employees in specific industries earning up to IDR 10 million per month may qualify for temporary PPh 21 relief. This impacts monthly withholding, not the annual progressive structure.

Using a personal income tax calculator effectively involves verifying its accuracy against official tax regulations and sample calculations, which builds trust and ensures correct withholding.

What you need to calculate personal income tax in Indonesia

Accurate payroll begins with complete employee data. Missing information is a common cause of incorrect PPh 21 withholding.

- NPWP (Nomor Pokok Wajib Pajak) status

- Monthly and annual income details

- Taxable allowances and benefits

- BPJS (Badan Penyelenggara Jaminan Sosial) employee contributions

- Pension contributions

- PTKP (Penghasilan Tidak Kena Pajak) status based on dependents

- Employment category

- Eligibility for PPh 21 DTP (Ditanggung Pemerintah) 2026 relief

These inputs allow a personal income tax calculator to produce reliable results.

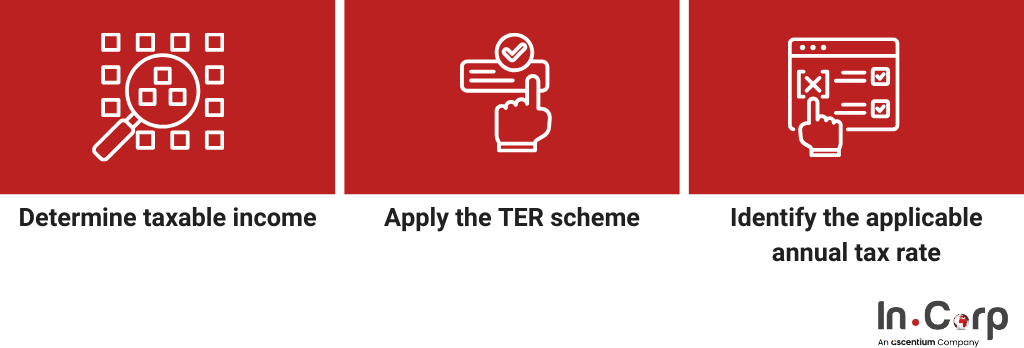

How income tax is calculated in Indonesia (PPh 21)

Following the sequence of calculating PPh 21-finding taxable income, applying the correct tax rate, and considering deductions-helps prevent common payroll mistakes like misapplying income brackets or deductions.

Determine taxable income

Taxable income is determined after applying all applicable deductions and exemptions.

Allowable deductions include:

- BPJS (Badan Penyelenggara Jaminan Sosial) employee contributions

- Approved pension contributions

- Job expense allowance within the official limit

Exemptions include:

- Non-taxable benefits within set thresholds

- Approved reimbursements

- PTKP (Penghasilan Tidak Kena Pajak) based on dependents

The result after these adjustments becomes the taxable income.

Apply the TER scheme

The TER (Tarif Efektif Rata-rata) method simplifies monthly withholding by applying a fixed effective rate based on income level. This reduces calculation complexity and minimizes year-end corrections. Many PPh 21 calculators include a TER mode for monthly payroll.

Identify the applicable annual tax rate

At the end of the year, taxable income is assessed using the Tarif Progresif PPh Pasal 17 structure. The monthly TER withholding is reconciled with the annual calculation to determine whether additional tax is due or a refund applies.

What income is not taxable in Indonesia

Not all components of employee compensation are subject to PPh 21. Understanding non-taxable income prevents over-withholding and improves payroll accuracy.

- PTKP (non-taxable threshold)

- Certain business reimbursements

- Non-taxable benefits within government limits

- Employer-paid BPJS contributions that meet the criteria

- Specific allowances categorized as non-taxable

- Industry-specific incentives or 2026 exemptions

Only the remaining taxable income should be entered into the personal income tax calculator for accurate PPh 21 calculation.

Are dividends taxed as personal income tax?

Dividends are treated separately from employment income and may be:

- Final tax, withheld at a fixed rate

- Non-final income, included in annual reporting using progressive rates

Dividends from Indonesian companies are often final, while foreign dividends may be subject to different rules depending on reinvestment and documentation.

Personal income tax obligations for expats in Indonesia

For expatriates, tax treatment depends on residency status. These are:

Tax residents (more than 183 days in Indonesia)

- Taxed on Indonesian income

- Certain foreign income may be taxed if brought into Indonesia

Non-residents

- Taxed only on Indonesian-sourced income

- Usually taxed at a flat rate instead of progressive brackets

Additional considerations include:

- Double taxation agreements (DTA)

- Employer withholding duties

- Reporting foreign-sourced income

A personal income tax calculator is suitable for employment income, but not for complex cross-border income.

Payroll Outsourcing in Indonesia: Building Continuity Through Compliance

Manage payroll in Indonesia with InCorp

Calculating PPh 21 becomes much easier when taxable income, deductions, TER rules, and progressive brackets are understood clearly. With complete data and updated knowledge of Indonesia’s payroll framework, companies can manage withholding more confidently.

A reliable personal income tax calculator helps support consistency, but human oversight remains essential to handle exemptions and exceptional cases.

InCorp Indonesia (an Ascentium Company) provides full-service payroll management to help businesses stay compliant with evolving tax regulations.

- End-to-end payroll processing, including monthly salary computation and statutory withholding

- Accurate PPh 21 calculations, aligned with updated rules, TER application, and year-end reconciliation

- Employee payslip management, with transparent and timely reporting

Fill out the form below to remove payroll-related uncertainty and stay focused on core activities.

Frequently Asked Questions

What is PPh 21 in Indonesia?

PPh 21 is the personal income tax withheld from employee earnings such as salaries, allowances, bonuses, and other compensation.

How is personal income tax calculated in Indonesia?

Tax is calculated by determining taxable income after deductions, then applying the applicable progressive tax rates or the TER method for monthly withholding.

What information is needed to calculate PPh 21 accurately?

Companies need employee income details, NPWP status, BPJS and pension contributions, PTKP status, and eligibility for any tax relief programs.

Are all types of employee income taxable under PPh 21?

No. Some components, such as certain benefits, reimbursements, and income within the PTKP threshold, may be considered non-taxable.

Can a personal income tax calculator replace proper payroll management?

A calculator helps estimate tax amounts, but accurate withholding still depends on correct data, updated regulations, and proper payroll review.

Get in touch with us.

What you'll get

A prompt response to your inquiry

Knowledge for doing business from local experts

Ongoing support for your business

Disclaimer

The information is provided by PT. Cekindo Business International (“InCorp Indonesia/ we”) for general purpose only and we make no representations or warranties of any kind.

We do not act as an authorized government or non-government provider for official documents and services, which is issued by the Government of the Republic of Indonesia or its appointed officials. We do not promote any official government document or services of the Government of the Republic of Indonesia, including but not limited to, business identifiers, health and welfare assistance programs and benefits, unclaimed tax rebate, electronic travel visa and authorization, passports in this website.