Capital gains tax in Indonesia is the income tax imposed on profits from the sale or transfer of assets such as shares, land, buildings, and business interests. Indonesia does not have a standalone capital gains tax system. Instead, capital gains are taxed under the Income Tax Law (UU PPh), as amended by the Harmonized Tax Law (UU HPP No. 7/2021), with the treatment depending on the type of asset sold.

Certain transactions may be subject to final tax on gross proceeds, while other gains are treated as taxable income and taxed at the applicable standard income tax rates, which may reach up to 35% for individuals.

Key Takeaways

- Indonesia does not have a standalone capital gains tax system; capital gains are taxed under the Income Tax Law and UU HPP No. 7/2021.

- Capital gains tax treatment depends on the asset type, with listed shares, property, unlisted shares, and non-resident asset sales taxed differently.

- Listed shares on the IDX are subject to 0.1% final tax, while land and building transfers are generally subject to 2.5% final tax.

- Gains from unlisted shares or other assets owned by residents are treated as taxable income and taxed at up to 35% for individuals or 22% for companies.

- Capital gains tax should be reviewed before asset sales, share transfers, or restructuring to avoid blocked transactions, penalties, withholding issues, and annual tax return mismatches.

Why capital gains tax mistakes can be costly

Foreign investors, property sellers, and business owners in Indonesia often misunderstand capital gains tax, leading to immediate financial consequences.

- Blocked transactions: Land, building, or listed-share transfers may be delayed until the final tax is paid and validated.

- Late-payment penalties: Underpaid gains may trigger interest of around 2% per month, plus assessment penalties.

- Withholding failures: If the buyer or counterparty fails to withhold tax, the resident party may be liable.

- Lost treaty relief: Non-residents without a Certificate of Domicile (CoD) may face the full 20% withholding tax.

- Annual return mismatches (SPT Tahunan): Unreported gains in the SPT Tahunan may increase the risk of DJP review or audit.

Capital gain tax rates in Indonesia (2026 updates)

Indonesia taxes capital gains based on the type of asset sold. For sellers, identifying the asset category is the first step to determining the right tax treatment.

| Asset Sold | Capital Gains Tax Treatment |

| Listed Shares on the IDX | 0.1% final tax on the gross transaction value, withheld by the broker |

| Founder Shares at IPO | Additional 0.5% final tax on the share value at listing |

| Land and Buildings | 2.5% final tax on the transaction value or government-assessed value, whichever is higher. A 1% rate may apply to low-cost housing. |

| Unlisted Shares or Other Assets Owned by Residents | Net gain is added to taxable income and taxed at the applicable income tax rate: up to 35% for individuals or 22% for companies. |

| Indonesian Assets Sold by Non-Residents | 5% final tax on gross proceeds, unless reduced by an applicable tax treaty. |

For assets taxed as ordinary income, individual taxpayers are subject to progressive income tax rates:

| Annual Taxable Income | Tax Rate |

| Up to IDR 60 million | 5% |

| Over IDR 60 million to IDR 250 million | 15% |

| Over IDR 250 million to IDR 500 million | 25% |

| Over IDR 500 million to IDR 5 billion | 30% |

| Over IDR 5 billion | 35% |

Resident companies are generally subject to a 22% corporate income tax rate. Qualifying public companies may access a reduced 19% rate if at least 40% of their shares are publicly held, and other requirements are met.

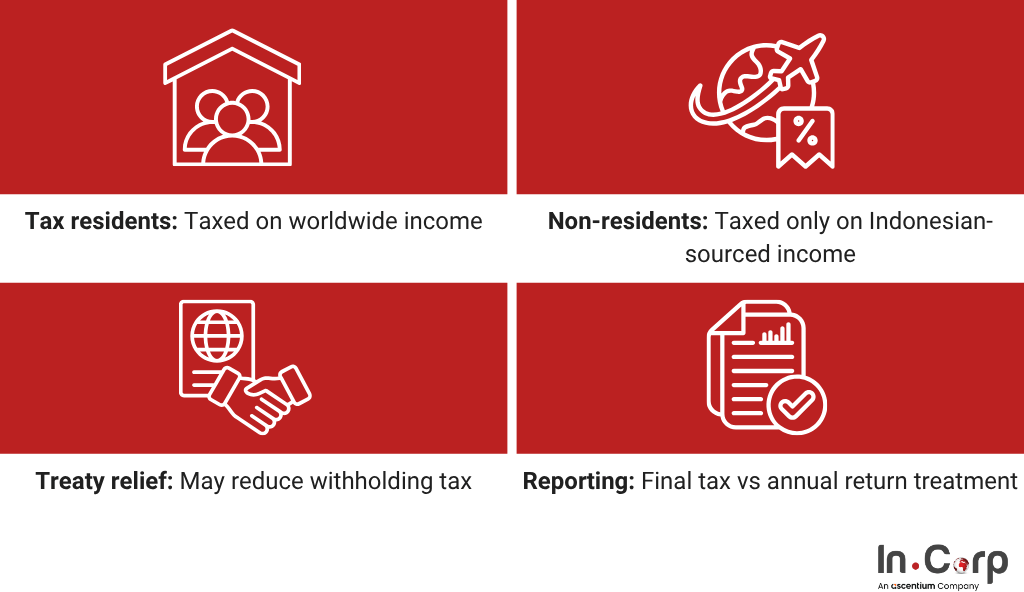

Capital gains tax for residents and non-residents

In Indonesia, capital gains tax treatment depends on the seller’s tax residency status. These are:

- Tax residents include Indonesian nationals and individuals who reside in Indonesia for more than 183 days within a 12-month period. They are generally taxed on worldwide income, including overseas gains, unless relief is available under a Double Taxation Agreement.

- Non-residents are generally taxed only on Indonesian-sourced income. This may include a 20% withholding tax under Article 26 or a 5% final tax on the gross proceeds from certain asset sales, unless a tax treaty provides a lower rate.

Indonesia uses a self-assessment tax system, meaning taxpayers are responsible for calculating, paying, and reporting their own tax liabilities. For final-tax assets such as listed shares and property, tax is usually settled at the time of the transaction. For other taxable gains, the income must be reported on the annual tax return.

Capital gains tax vs VAT and BPHTB in Indonesia

Sellers often confuse capital gains tax with other transaction-related taxes. Each tax is a separate obligation with its own taxpayer, rate, and reporting timeline.

| Tax | When It Applies | Rate | Who Usually Pays | Reporting/Payment Timing |

| Capital Gains Tax | Profit or proceeds from asset disposal | 0.1% / 2.5% / up to 35% | Seller | Usually settled at the transaction stage for final-tax assets, or reported in the annual tax return for assessable gains |

| VAT / PPN | Sale of taxable goods or services | 11% effective (12% on luxury goods) | Taxable entrepreneur/seller, charged to the buyer | The monthly VAT return is filed and paid by the end of the following month |

| Land & Building Transfer Duty (BPHTB) | Buyer’s acquisition of land or building rights | Up to 5% | Buyer | Usually paid before the land or building title transfer is completed |

A property sale, for example, can trigger the seller’s 2.5% final income tax and the buyer’s BPHTB on the same transaction.

Key tax reporting deadlines

- Individual annual tax return (SPT Tahunan): Due by 31 March of the following year.

- Corporate annual tax return (SPT Tahunan Badan): Due by the end of the fourth month after the financial year, typically 30 April.

- Withholding tax: Generally paid by the 10th and reported by the 20th of the following month.

- Monthly VAT return (SPT Masa PPN): Filed and paid by the end of the following month.

The non-taxable income threshold (PTKP) remains IDR 54 million per year for a single taxpayer, with additional allowances for spouses and dependents.

Mastering Corporate Taxation in Indonesia

Get capital gains tax right the first time

Incorrect or delayed reporting of capital gains tax can lead to costly penalties and difficulties in correction, emphasizing the need for accurate compliance to keep readers engaged with proper procedures.

InCorp Indonesia (an Ascentium Company) supports companies and foreign investors through our tax consulting services with:

- Transaction tax review

- Capital gains tax calculation

- Withholding and treaty assessment

- Tax payment and validation support

- Corporate tax reporting assistance

Planning a share transfer, asset sale, or corporate restructuring in Indonesia? Fill out the form below to ensure your capital gains tax is calculated, paid, and reported correctly.

Frequently Asked Questions

What is the capital gain tax rate in Indonesia?

It depends on the asset: 0.1% on listed shares, 2.5% on land and buildings, and progressive rates up to 35% on other assets for individuals (22% for companies).

Do foreigners pay capital gain tax in Indonesia?

Yes. Non-residents pay 5% on gross proceeds from Indonesian asset sales or 20% withholding on other gains, unless a tax treaty reduces the rate.

Is capital gain tax on property final in Indonesia?

Yes. The 2.5% tax on land and building transfers is a final tax based on the transaction or government-assessed value, whichever is higher.

How are listed share sales taxed?

A 0.1% final tax is automatically withheld by the broker on the gross sale value, regardless of whether the trade was profitable.

When must capital gains be reported?

Final-tax gains are settled at the transaction. Assessable gains are declared in the annual return — due 31 March (individuals) or 30 April (companies).

Get in touch with us.

What you'll get

A prompt response to your inquiry

Knowledge for doing business from local experts

Ongoing support for your business

Disclaimer

The information is provided by PT. Cekindo Business International (“InCorp Indonesia/ we”) for general purpose only and we make no representations or warranties of any kind.

We do not act as an authorized government or non-government provider for official documents and services, which is issued by the Government of the Republic of Indonesia or its appointed officials. We do not promote any official government document or services of the Government of the Republic of Indonesia, including but not limited to, business identifiers, health and welfare assistance programs and benefits, unclaimed tax rebate, electronic travel visa and authorization, passports in this website.

Verified by

Heldy Narua

Senior External Finance Manager at InCorp Indonesia

Heldy, with seven years of experience, leads InCorp Indonesia’s External Finance team, specializing in reliable Payroll Outsourcing and Finance Management solutions. She has an Accounting and Business Administration degree from Sampoerna University and Oregon State University. She is certified with Brevet AB, highlighting her technical expertise and commitment to client success.