Many foreign businesses in Indonesia pay more withholding tax than necessary because their tax treaty position is not properly reviewed. Others assume they qualify for treaty relief, only to find later that the documents, structure, or substance behind the claim do not hold up.

Under the updated MoF Regulation No. 112 of 2025, treaty claims in Indonesia are no longer just about filing the right form. Companies must now demonstrate genuine substance behind the claim, which helps the audience feel assured about proper compliance and reduces uncertainty.

Key Takeaways

- Tax treaty benefits in Indonesia can reduce withholding tax on dividends, interest, royalties, and other cross-border income.

- Under MoF Regulation No. 112 of 2025, treaty claims must be supported by substance, not only forms or documentation.

- Foreign taxpayers must generally provide a valid Certificate of Domicile, submit the correct DGT form, and pass substance tests to claim treaty benefits.

- Treaty claims may fail if the foreign entity lacks genuine business activity, applies the wrong treaty treatment, or fails to meet documentation timing requirements.

- Businesses with foreign shareholders, cross-border financing, royalties, or outbound payments should review their treaty position early to avoid higher withholding tax and disputes.

Can a tax treaty reduce your withholding tax in Indonesia?

Yes. A tax treaty may reduce withholding tax on dividends, interest, royalties, and other cross-border income paid by Indonesia entities to foreign recipients. This can directly affect the total tax cost of a transaction.

For example, without treaty relief, a Singapore holding company that receives dividends from an Indonesian subsidiary could be subject to a 20% Indonesian withholding tax, in addition to any domestic taxes imposed by Singapore. However, a tax treaty can lower the Indonesian withholding tax rate to as low as 10%, resulting in substantial savings on significant dividend distributions.

What is a tax treaty?

A tax treaty (Double Tax Avoidance Agreements) is an agreement between two countries that helps prevent the same income from being taxed twice. In Indonesia, it is commonly used to determine whether a foreign taxpayer is eligible for reduced withholding tax rates on certain income.

For business purposes, the key question is not just whether a treaty exists, but whether it can be applied correctly to the specific payment, entity, and structure involved.

Who can claim tax treaty benefits in Indonesia?

Not every foreign taxpayer automatically qualifies for treaty benefits. In practice, treaty access depends on proper documentation, such as tax residence, a valid Certificate of Domicile (CoD), and sufficient substance, thereby enabling the audience to manage their compliance with confidence.

This means that having an entity in a treaty partner country is not enough on its own. The company must also be able to support that the arrangement is genuine and that the treaty claim is not being used only to obtain a lower tax rate.

Not sure whether your home country qualifies? Our tax consultants can verify your treaty eligibility and help you navigate the complexities, giving you confidence and peace of mind in your compliance approach.

What changed under MoF Regulation No. 112 of 2025

MoF Regulation No. 112 of 2025 changes how treaty benefits are applied in Indonesia. The main shift is clear: treaty claims now require a stronger review of the foreign taxpayer’s actual eligibility, not just the paperwork.

For foreign taxpayers (WPLN)

Under the new regulations:

- One unified substance test now applies to all Indonesian-sourced income

- Withholding agents must assess real eligibility, not just document completeness

- Full domestic withholding applies if treaty conditions are not met

- Treaty benefits may be denied under the new Principal Purpose Test (PPT)

For Indonesian taxpayers (WPDN) and withholding agents

According to the new regulations:

- Certificate of Domicile (CoD) applications now run through Coretax

- The CoD format is simpler than before

- Withholding agents must report through Coretax and keep supporting records

- Tax slips must still be issued, even when the treaty reduces withholding to zero

In short, older treaty practices that relied mainly on forms may no longer be enough.

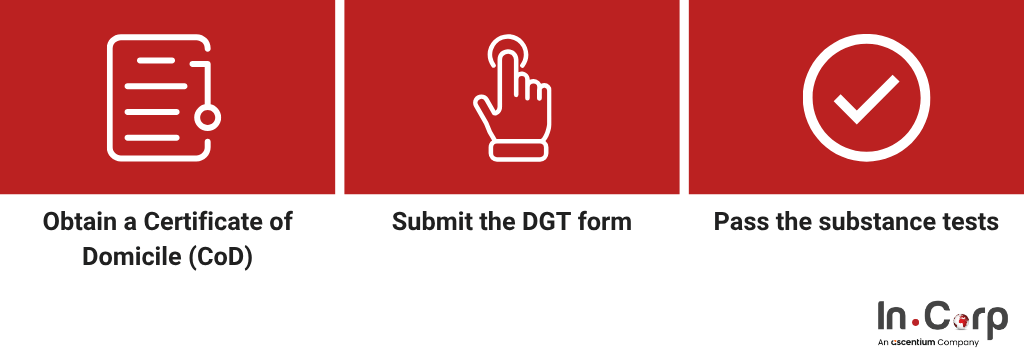

How do you claim tax treaty benefits in Indonesia?

Claiming treaty benefits involves three key steps: obtaining a Certificate of Domicile, submitting the correct DGT form, and passing substance tests to verify genuine business activity.

Obtain a Certificate of Domicile (CoD)

For foreign taxpayers, this means obtaining a CoD from the tax authority in their home country. For Indonesian taxpayers, the application is now handled through Coretax.

Submit the DGT form

The relevant DGT Form must be submitted to the Indonesian withholding agent before or at the time the income is paid. This form requires the foreign taxpayer to confirm its residency status and to provide evidence that it is not using the treaty abusively.

Pass the substance tests

Under MoF 112, this includes whether the entity has genuine business activity, sufficient staff and assets, real control over its income, and a structure not primarily set up to obtain treaty benefits.

If these conditions are not met, the treaty claim may be denied, and the full domestic withholding tax rate may apply.

Why do tax treaty claims fail?

Most treaty claims fail not because a treaty does not exist, but because the business is not ready to support it properly. Common problems include:

- Assuming the foreign entity automatically qualifies

- Relying on a CoD without reviewing the substance

- Using the wrong treaty treatment for the income type

- Missing documentation timing

- Failing to align the claim with withholding and reporting obligations

For a business, these are not minor administrative errors. They can lead to higher withholding tax, disputes over tax costs, delayed transactions, and unnecessary exposure during a review.

When should a business use a tax consultant for tax treaty review?

A business should consider tax consulting support when the treaty claim involves a higher value, more risk, or a more complex structure. This is especially relevant when:

- Your Indonesian income flows through a holding or multi-tier group structure

- You are making a first-time treaty claim

- Your group has recently restructured or completed an M&A activity

- You are already dealing with an audit, objection, or dispute

- The dividend, interest, or royalty amounts involved are substantial

In these situations, reviewing the treaty position early is often more efficient than fixing it later.

Mastering Corporate Taxation in Indonesia

How InCorp helps businesses review tax treaty risk

A tax treaty can reduce withholding tax, but only if the claim is properly structured and supported. Under MoF 112, businesses should no longer rely solely on forms.

InCorp Indonesia (an Ascentium Company), with our tax consulting services, can help businesses to:

- Review treaty eligibility

- Assess withholding tax exposure

- Assist in supporting documents and substance behind the foreign entity receiving the income

When the structure is more complex, InCorp can also help businesses evaluate whether the current arrangement remains appropriate under the updated regulations.

If your company has foreign shareholders, cross-border financing, royalty arrangements, or other outbound payments from Indonesia, now is the right time to review whether your treaty position still works.

Fill out the form below for a tax treaty eligibility assessment and practical review of your withholding tax exposure.

Frequently Asked Questions

What is the difference between a tax treaty and a DTAA?

They are the same thing. 'Tax treaty' and 'Double Tax Avoidance Agreement (DTAA)' are interchangeable terms. In Indonesia, these are sometimes also called P3B (Perjanjian Penghindaran Pajak Berganda).

How many countries have a tax treaty with Indonesia?

Indonesia has signed Double Tax Avoidance Agreements with more than 71 countries, covering most major economies across Asia, Europe, North America, the Middle East, and Africa.

What changed under MoF Regulation No. 112 of 2025?

MoF-112, which came into force on 31 December 2025, replaced the previous DGT Regulations No. 28/PJ/2018 and No. 25/PJ/2018. Key changes include: a simplified online CoD process via CoreTax, a unified substantive eligibility test replacing the standalone beneficial owner test, enhanced obligations on Indonesian withholding agents to assess treaty eligibility (not just check paperwork), and the incorporation of the Principal Purpose Test (PPT) principles to deny treaty benefits in abusive arrangements.

What is a DGT Form and when do I need one?

The DGT Form is submitted by a foreign taxpayer (WPLN) to the Indonesian withholding agent to claim tax treaty benefits. It confirms the foreign taxpayer's residency in a treaty partner country, their beneficial ownership of the income, and their compliance with anti-abuse requirements. It must be submitted before or at the time income is paid. Certain recipients — including governments, central banks, and institutions explicitly recognised under the relevant treaty — are exempt from this requirement.

What happens if my Certificate of Domicile expires?

Under MoF-112, a CoD issued through the DGT's CoreTax system is valid until 31 December of the issuance year. If it expires, the Indonesian withholding agent must apply the standard 20% domestic withholding rate until a new CoD is obtained. Annual renewal is now a standard compliance requirement.

Can treaty benefits be claimed retroactively?

MoF-112 clarifies that treaty benefits can still be claimed if the DGT Form is submitted during a tax audit, objection, or assessment review — as long as the substantive treaty requirements are otherwise satisfied. However, retroactive claims are more complex and carry greater risk than getting the process right from the outset.

What is the Principal Purpose Test (PPT)?

The PPT is an anti-abuse provision incorporated into MoF-112 in line with OECD BEPS standards. It allows the DGT to deny treaty benefits where it is reasonable to conclude that one of the principal purposes of an arrangement or transaction is to obtain treaty benefits. This is distinct from outright tax evasion — even arrangements with a legitimate business purpose can fail the PPT if treaty benefit optimisation is among the principal motivations.

Do I need a tax consultant to claim Indonesia tax treaty benefits?

For straightforward situations — a single entity in a treaty partner country receiving dividends from one Indonesian subsidiary, with clear economic substance — the process is manageable with good internal documentation. However, for complex group structures, post-restructuring positions, or where amounts are material, professional tax consulting support typically pays for itself through avoided errors, reduced audit risk, and optimised treaty positioning.

Get in touch with us.

What you'll get

A prompt response to your inquiry

Knowledge for doing business from local experts

Ongoing support for your business

Disclaimer

The information is provided by PT. Cekindo Business International (“InCorp Indonesia/ we”) for general purpose only and we make no representations or warranties of any kind.

We do not act as an authorized government or non-government provider for official documents and services, which is issued by the Government of the Republic of Indonesia or its appointed officials. We do not promote any official government document or services of the Government of the Republic of Indonesia, including but not limited to, business identifiers, health and welfare assistance programs and benefits, unclaimed tax rebate, electronic travel visa and authorization, passports in this website.

Verified by

Heldy Narua

Senior External Finance Manager at InCorp Indonesia

Heldy, with seven years of experience, leads InCorp Indonesia’s External Finance team, specializing in reliable Payroll Outsourcing and Finance Management solutions. She has an Accounting and Business Administration degree from Sampoerna University and Oregon State University. She is certified with Brevet AB, highlighting her technical expertise and commitment to client success.