Filing an annual corporate tax return (SPT Tahunan Badan) in Indonesia can result in an unexpected tax obligation known as PPh 29 underpayment. This happens when a company’s actual taxable income exceeds the income used to calculate its monthly PPh 25 installments. The remaining tax gap must be paid before April 30 to avoid interest penalties.

For foreign-invested companies (PT PMA), this risk can be higher. Revenue growth, new business activities, product changes, or currency fluctuations can increase taxable income beyond the previous year’s estimate. Without regular tax monitoring, companies may face large PPh 29 payments at year-end.

To avoid unexpected year-end tax payments, companies need to understand how PPh 29 is calculated, when it must be paid, and what steps to take to monitor the risk before filing.

Key Takeaways

- PPh 29 is the remaining corporate income tax payable when a company’s annual tax due is higher than its prepaid tax credits and PPh 25 installments.

- Corporate PPh 29 underpayment must be paid before submitting the annual corporate tax return, with April 30 as the usual filing deadline for calendar-year taxpayers.

- Indonesia’s standard corporate income tax rate is 22% of net taxable income, while eligible SMEs may use the 0.5% final tax regime.

- PPh 29 risk can increase when revenue grows, new business activities are added, tax credits are lower than expected, or fiscal corrections increase taxable income.

- Companies should review deductible expenses, tax credits, PPh 25 installments, and transfer pricing adjustments before filing to avoid underpayment and penalties.

Corporate PPh 29 at a glance

| Requirement | Details |

| Who It Applies To | PT, CV, Firma, Koperasi, PT PMA, and permanent establishments (BUT) |

| Legal Basis | Income Tax Law No. 36/2008, amended by UU HPP No. 7/2021 |

| When PPh 29 Applies | When the annual tax payable exceeds prepaid tax credits and PPh 25 installments |

| Standard Corporate Tax Rate | 22% of taxable income |

| SME Final Tax Rate | 0.5% final tax for eligible companies with gross revenue up to IDR 4.8 billion |

| Filing Deadline | 4 months after the fiscal year-end, usually April 30 |

| Payment Deadline | Before submitting the annual corporate tax return |

| Late Payment Penalty | Interest and administrative penalties may apply, so companies should prioritize timely payments to avoid accumulating penalties |

| Payment Method | DJP Online e-billing, paid through bank, ATM, or internet banking |

What is PPh 29?

PPh 29 is the remaining income tax that must be paid when a company’s annual tax payable is higher than the tax already paid during the year.

These prepaid taxes may include:

- PPh 22 from import or certain business transactions

- PPh 23 from dividends, royalties, interest, or service payments

- PPh 25 monthly corporate income tax installments

In simple terms, PPh 29 is an underpayment. It is not a penalty, but the unpaid balance of the company’s income tax obligation for the fiscal year.

Why corporate PPh 29 happens

Monthly PPh 25 installments are usually based on the previous year’s annual tax return and divided into 12 payments. Because this calculation looks backward, the installments may no longer match the company’s current business performance.

PPh 29 underpayment can become larger when:

- Revenue or profit increases beyond the previous year’s estimate.

- New business activities are added, such as new contracts, products, or services.

- Tax credits are lower than expected, including PPh 22 or PPh 23.

- Non-deductible expenses are found during the fiscal closing, increasing taxable income.

- Transfer pricing adjustments are made, especially for related party transactions.

Current corporate income tax rates in Indonesia

Under UU HPP No. 7/2021, Indonesia’s standard corporate income tax rate is 22% of net taxable income.

| Entity Type/Revenue | Applicable Tax Rate |

| Gross revenue above IDR 50 billion | 22% of net taxable income |

| Gross revenue between IDR 4.8 billion and IDR 50 billion | Blended rate: 11% on the eligible portion and 22% on the remaining taxable income |

| Gross revenue up to IDR 4.8 billion | 0.5% final tax on gross revenue, subject to eligibility under PP 55/2022 |

| Publicly listed companies meeting PMK 40/2023 criteria | 19%, or 3% lower than the standard corporate tax rate |

Note for PT PMA: Foreign-invested companies generally follow the same 22% standard corporate tax rate. However, dividend payments to foreign shareholders, related-party transactions, and tax treaty benefits can affect the company’s effective tax exposure. These areas often require further tax review before filing or profit distribution.

Need to review your PT PMA tax position? Talk to our team.

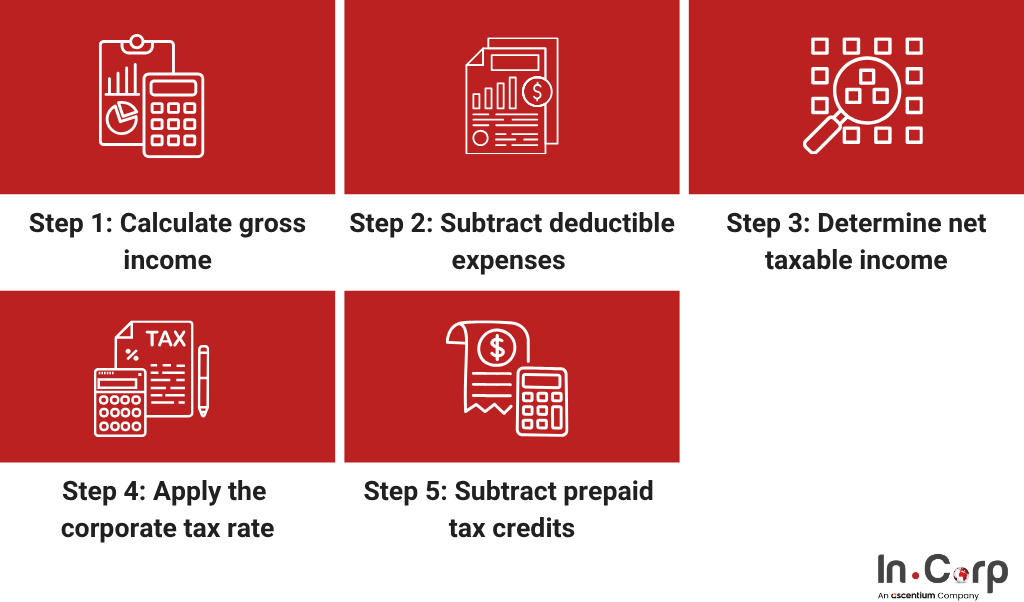

How to calculate corporate PPh 29

For companies with gross revenue above IDR 50 billion, PPh 29 is calculated by comparing the annual tax payable with the tax credits paid during the year, helping companies clearly understand their potential underpayment.

Step 1: Calculate gross income

Add all taxable income, including sales, service revenue, and other business income.

Step 2: Subtract deductible expenses

Deduct business expenses used to earn, collect, and maintain income, often referred to as Biaya 3M. Non-tax-deductible expenses must be added back through a fiscal correction.

Step 3: Determine net taxable income

After deductible expenses and fiscal corrections, the company arrives at its net taxable income (PKP).

Step 4: Apply the corporate tax rate

Calculate annual corporate tax payable using the standard 22% rate.

Tax payable = 22% × net taxable income

Step 5: Subtract prepaid tax credits

Deduct tax credits already paid during the year, such as PPh 22, PPh 23, and PPh 25 installments.

PPh 29 = tax payable − prepaid tax credits

When the final amount is positive, the company has a PPh 29 underpayment that must be paid before submitting the annual corporate tax return.

Deductible vs non-deductible expenses under UU HPP

Correctly classifying expenses is important because it affects fiscal corrections and the final PPh 29 calculations.

Deductible expenses

These are expenses that can generally reduce taxable income if they are related to business activities:

- Employee benefits that are properly structured and documented

- Meals and beverages are provided for all employees

- Transportation or operational support related to work

- Health facilities or medical support for employees

- Safety equipment and work uniforms

- Other expenses used to obtain, collect, and maintain taxable income

Non-deductible expenses

These are expenses that generally cannot reduce taxable income and must be added back through fiscal correction:

- Personal expenses not related to business activities

- Excessive or unsupported entertainment expenses

- Expenses without proper invoices or documentation

- Penalties and sanctions that are not tax-deductible

- Benefits or facilities that are not properly classified under tax rules

For PPh 29, misclassification can create two risks: overpayment, which affects cash flow, or underpayment, which results in additional tax and interest.

How to pay corporate PPh 29

Corporate PPh 29 underpayment is paid through DJP Online e-Billing before the annual corporate tax return is submitted.

In general, companies need to:

- Log in to DJP Online using the company’s NPWP account.

- Create a billing code for the PPh 29 payment.

- Enter the correct tax period and underpayment amount.

- Complete the payment through an available banking channel.

- Keep the payment receipt, or Bukti Penerimaan Negara (BPN), for annual tax filing records.

While the payment process may seem straightforward, errors in calculation, tax classification, or filing timing can create unnecessary delays.

If your company needs support reviewing its PPh 29 position, InCorp can help ensure the process is handled correctly before submission. Talk to our team ->

Key deadlines and penalties

Corporate PPh 29 must be paid before the annual corporate tax return is submitted. For companies using the calendar year, the filing deadline is generally April 30.

| Action | Deadline |

| Pay PPh 29 underpayment | Before submitting the annual corporate tax return |

| File SPT Tahunan Badan | No later than April 30 for calendar-year taxpayers |

| Request filing extension | Before the filing deadline, make an estimated tax payment if applicable |

Late payment may result in monthly interest on the unpaid tax amount at the rate set by the Minister of Finance. If the annual corporate tax return is not filed, companies may also face a fixed administrative penalty of IDR 1,000,000, in addition to any interest on any underpayment.

To avoid penalties, companies should calculate and settle PPh 29 before filing the annual corporate tax return.

Mastering Corporate Taxation in Indonesia

Prepare your corporate tax filing with confidence

Managing corporate tax compliance in Indonesia demands both technical knowledge and operational consistency. InCorp Indonesia (an Ascentium Company) helps businesses manage annual tax obligations accurately and on time with:

- Annual SPT Tahunan Badan preparation: From bookkeeping review to final filing

- PPh 25 installment optimization: Ensuring monthly payments track actual income

- Transfer pricing compliance: TP documentation, benchmarking studies, and APA applications

- Tax dispute resolution: Representation before the DJP for objections, appeals, and audits

- Tax health checks: Identifying PPh 29 exposure and correction opportunities before the SPT deadline

With offices in Jakarta, Bali, Surabaya, Semarang, and Batam, our team serves Indonesian companies and PT PMA across all major industries.

Schedule a free consultation with our tax team →

Frequently Asked Questions

What is PPh 29 in Indonesia?

PPh 29 is the remaining corporate income tax that must be paid when a company’s annual tax payable is higher than the tax credits and monthly PPh 25 installments already paid during the year. It is an underpayment, not a penalty, and must be settled before filing the annual corporate tax return.

When does corporate PPh 29 underpayment happen?

Corporate PPh 29 underpayment happens when actual taxable income is higher than the income used to calculate monthly PPh 25 installments. This can occur due to revenue growth, lower tax credits, non-deductible expenses, transfer pricing adjustments, or new business activities.

How is corporate PPh 29 calculated?

Corporate PPh 29 is calculated by applying the corporate income tax rate to net taxable income, then subtracting prepaid tax credits such as PPh 22, PPh 23, and PPh 25 installments. If the result is positive, the company has a PPh 29 underpayment.

When must PPh 29 be paid in Indonesia?

PPh 29 must be paid before the annual corporate tax return is submitted. For calendar-year taxpayers, the annual corporate tax return deadline is generally April 30, so the PPh 29 underpayment must be settled before that filing.

How can companies reduce unexpected PPh 29 exposure?

Companies can reduce unexpected PPh 29 exposure by monitoring taxable income throughout the year, reviewing deductible and non-deductible expenses, optimizing PPh 25 installments, checking tax credits, and conducting a tax health check before the annual filing deadline.

Get in touch with us.

What you'll get

A prompt response to your inquiry

Knowledge for doing business from local experts

Ongoing support for your business

Disclaimer

The information is provided by PT. Cekindo Business International (“InCorp Indonesia/ we”) for general purpose only and we make no representations or warranties of any kind.

We do not act as an authorized government or non-government provider for official documents and services, which is issued by the Government of the Republic of Indonesia or its appointed officials. We do not promote any official government document or services of the Government of the Republic of Indonesia, including but not limited to, business identifiers, health and welfare assistance programs and benefits, unclaimed tax rebate, electronic travel visa and authorization, passports in this website.

Verified by

Heldy Narua

Senior External Finance Manager at InCorp Indonesia

Heldy, with seven years of experience, leads InCorp Indonesia’s External Finance team, specializing in reliable Payroll Outsourcing and Finance Management solutions. She has an Accounting and Business Administration degree from Sampoerna University and Oregon State University. She is certified with Brevet AB, highlighting her technical expertise and commitment to client success.